By: Tia Politi, ORHA President

March 8, 2022

I am often asked by rental owners how their tenant’s renter’s insurance can help them, or how it helps their residents. While there is some variation in policy coverage, two of the best reasons to require or encourage your residents to obtain it are: accidents and liability coverage.

Accidents happen. I once had a tenant who accidentally started a kitchen fire. Thank goodness she was insured. The damage claim exceeded $70,000 for damage to the home and her belongings. Without renter’s insurance, my owner’s insurance would have kicked in, but the resident would have been potentially liable for the deductible and any premium increase associated with the accident, and her personal property would not have been covered. Also, the owner’s insurance company may have sought to subrogate the claim to her. Instead, the home was restored and her damaged belongings replaced.

During a windstorm, a large tree fell on one of our resident’s homes. The owner’s insurance is covering the cost of repairing the damage to the home, but not damage to the resident’s belongings or car. Fortunately, the resident had insurance and was made financially whole.

One of my dear friends lived in a rental that burned up while they were away on a trip. It was a tragic event and they lost their beloved family dog as well as irreplaceable family mementos, but her family could have lost much more if they did not have renter’s insurance. Their insurance company paid for their hotel and temporary housing while they located a new home, and gave them money to purchase replacement clothing and household goods. Without renter’s insurance their distress would have been compounded exponentially.

A former client had their insurance attached by a claim from a neighbor. Their tenants’ dog had previously been considered friendly, but one day a neighbor girl who had interacted with the dog many times without incident, leaned down to pet the dog, and without warning it bit her in the face. She required extensive medical attention and plastic surgery. The residents had no renter’s insurance so the entire claim went against the owners’ insurance resulting in a huge premium increase. If the residents had renter’s insurance their policy would have been attached first, possibly eliminating any involvement of the owners’ insurance company. While the insurance company tried to subrogate to the tenants, they were very low income so there was nothing to go after.

Another benefit to tenants is the theft coverage that comes with a renter’s insurance policy. My daughter’s renter’s insurance had lapsed for a short time after she moved into a new unit, when her $2000 laptop was stolen out of her boyfriend’s car. His auto insurance did not cover that, but her renter’s insurance would have. Thefts from the dwelling unit itself may also be covered.

One of my tenants made a claim on her renter’s insurance policy when there was an electrical problem with the transformer serving the property that caused the power to surge dramatically, frying out her computer and the control panel for her washing machine. For some reason the utility company reimbursed me for the electrical repair to the home caused by their faulty transformer, but not my tenant’s damaged goods. She wasn’t interested in a legal battle with them and instead received reimbursement from her renter’s insurance policy.

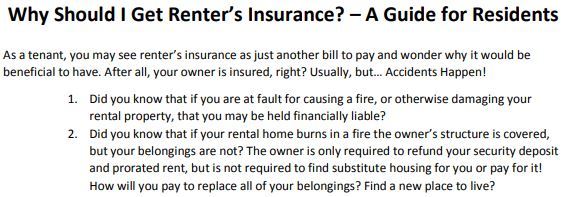

Kids throw baseballs through windows, people think their car is in reverse when it’s it drive and back into garage doors, tenants forget to lock doors and get robbed, previously friendly dogs bite people, candles set houses on fire – life is decidedly unpredictable, that’s why we should all be insured and why residents should be too. Many residents don’t know all the very good ways that renter’s insurance can benefit them, so I have created a one-page handout, Why Should I Get Renter’s Insurance? A Guide for Residents, that is available on my website (www.tiapoliti.com). Feel free to use it to educate your residents if you wish.

Can I really require my tenants to get renter’s insurance?

Yes, but there are exceptions.

What do I need to do to require Renter’s Insurance?

Before entering a new tenancy, you must advise an applicant in writing of a requirement to obtain and maintain renter’s liability insurance and the amount of insurance required and provide a reasonable written summary of the exceptions to this requirement. The Application to Rent – ORHA form #S1 has the required disclosure language, but you need to check the box to indicate the requirement on the form. If the applicant meets the income threshold, you may require an applicant to provide documentation of renter’s liability insurance coverage before the tenancy begins. The amount of coverage may not exceed $100,000 per occurrence or the customary amount required by landlords for similar properties with similar rents in the same rental market, whichever is greater.

For an existing month-to-month tenancy, you may amend a written rental agreement to require renter’s liability insurance after giving the tenant at least 30 days’ written notice of the requirement along with the disclosure stating the exceptions to your request. If the tenant does not obtain renter’s liability insurance within the 30-day period, you may terminate the tenancy for cause and the tenant has the opportunity to cure the cause or the tenancy terminates. Use Law Change Addendum – ORHA form #60 to implement the change with existing month-to-month tenancies. The form includes all the required language and allows you to update other law changes without requiring that the tenants sign a new agreement. If the tenant does not obtain renter’s insurance within the 30-day period, you may terminate the tenancy for cause, and the tenant has the opportunity to cure the cause by purchasing the required policy.

For a fixed-term lease where it was not required it at the outset, you must wait to implement the requirement until the expiration of the lease; however, you can and should send the notice of change in terms before the lease expires so that you may lawfully require it upon expiration of the lease if the tenancy is to continue.

You may require that a tenant obtain or maintain renter’s liability insurance only if you obtain and maintain comparable liability insurance. You must provide evidence of your insurance upon request. The written rental agreement must include a description of the requirements and exceptions to the requirements of a landlord’s right to require renter’s insurance.

What kind of coverage can I require? How will I know if the tenants maintain the policy? What can I do if they cancel the policy?

The landlord may require that qualifying tenants maintain a minimum of $100,000 in liability coverage and name the landlord as an interested party on the policy (some insurance companies call this a Certificate Holder) authorizing the insurer to notify the landlord of:

- Cancellation or nonrenewal of the policy

- Reduction of policy coverage

- Removal of the landlord as an Interested Party

With the proper language in your lease or addenda, failure to maintain the policy as required would become a lease violation and you could enforce the requirement by serving a Notice of Termination with Cause – ORHA form #38, requiring the tenant to cure the deficiency within the time allowed by law (14 days or longer depending on your method of service) or the tenancy would terminate within the time allowed by law (30 days or longer depending on your method of service).

The statute specifies that neither a landlord nor a tenant shall make unreasonable demands that have the effect of harassing the other with regard to providing documentation of insurance coverage, so don’t badger the tenants about it, just serve a notice.

Can I require tenants to use a specific insurer?

No.

When can’t I require renter’s insurance?

A landlord may not require a tenant to obtain or maintain renter’s liability insurance if the household income of the tenant is equal to or less than 50 percent of the area median income, adjusted for family size as measured up to a five-person family.

Visit https://www.huduser.gov/portal/datasets/il/il2019/2019summary.odn to determine what the income threshold is for your county and household size.

A landlord may not require a tenant to obtain or maintain renter’s liability insurance if the dwelling unit of the tenant has been subsidized with public funds, including federal or state tax credits, federal block grants authorized in the HOME Investment Partnerships Act under Title II of the Cranston-Gonzalez National Affordable Housing Act, as amended, or the Community Development Block Grant program authorized in the Housing and Community Development Act of 1974, as amended, project-based federal rent subsidy payments under 42 U.S.C. 1437f and tax-exempt bonds, but not including tenant-based federal rent subsidy payments under the Housing Choice Voucher Program authorized by 42 U.S.C. 1437f or any other local, state or federal rental housing assistance, or a unit that is not subsidized even if the unit is on premises in which some dwelling units are subsidized.

Even when you have a low-income resident whose income is below the threshold, or whose unit is exempt, however, there may be circumstances under which you can require them to carry renter’s insurance, such as an allowance for a pet or a pool. And even though owners may not require insurance in some cases, nothing says you can’t recommend it. Many times, when I explain to a tenant why they should have renter’s insurance, they choose to get it anyway to protect themselves. And it’s cheap - $7 to $20 per month on average added to an auto policy. Stand-alone policies may also be purchased.

Requiring renter’s insurance when it would be illegal to do so may incur a penalty of the tenant’s actual damages or $250, whichever is greater.

Can I make a claim against my tenant’s policy?

In many cases, yes. The claim must be for damages or costs for which the tenant is legally liable and not for damages or costs that result from ordinary wear and tear, acts of God or the conduct of the landlord; the claim is greater than the security deposit of the tenant, if any; and the landlord provides a copy of the claim to the tenant contemporaneous with filing the claim with the insurer. One ROA member who just found out she could claim against the renter’s policy submitted a claim that was honored after the work had been done; another negotiated a settlement for damages with the tenant’s insurer. Just remember the one-year statute of limitations. Also, know that if you file a frivolous claim against the renter’s liability insurance of a tenant, the tenant may recover their actual damages plus $500.

The Takeaway

You can and should require renter’s insurance, but just like everything in landlord-tenant law, there are specific rules to follow. Know the rules and it’s easy-peasy, don’t and you’ll pay the price.

This column offers general suggestions only and is no substitute for professional legal counsel. Please consult an attorney for advice related to your specific situation.